To the uninitiated, it may not be clear what the difference between Venmo and PayPal actually is.

Scratch that:

Even to those who ARE familiar with both, the differences may not be clear.

After all, PayPal and Venmo both let you send and receive money. Except, PayPal has been around forever, and Venmo is new.

Oh, and PayPal owns Venmo.

The short version is that PayPal is more complicated than Venmo. Yes, outwardly they seem very similar:

But in reality, PayPal is branching out into more and more different kinds of services. In many ways PayPal is starting to resemble a bank.

Okay, yes, they both serve those same fundamental needs. But even then, the question is, which one is better at it?

And aside from that, which one is better for you if you’re a freelancer? Running a small shop online? Or if you just want an easy digital wallet?

Let’s figure it out.

First up, the thing we all care about:

Pricing

I’ll spoil things a little bit early on: the basic services for both Venmo and PayPal are similar. It’s not that surprising, since PayPal owns Venmo.

But there are still some differences, and they relate to the different features offered by both.

So let’s cover Venmo first. How much does Venmo cost?

…Nothing.

Okay, obviously Venmo has to earn money somehow. But the service itself is free to install and use.

Even better, Venmo doesn’t charge fees for most of the basic services.

Here’s what those basic services are:

Sending money from a linked bank account, debit card, or Venmo balance; receiving money to your Venmo balance or withdrawing into your Venmo balance; using the standard transfer to your bank account.

That all sounds too good to be true, I know.

Here’s what Venmo WILL charge fees for:

A standard withdrawal is free, but takes a business day. If you need the money immediately, you can do an instant withdrawal, which costs 1% of the amount.

Additionally, while sending money to people using your existing balance, debit card, or bank account IS free, using a credit card incurs a 3% charge.

For the most part, that’s it on pricing. But there are some other minor details for special users:

Users who are using the Venmo Card, or Venmo Mastercard—which is part of Venmo’s step into other services—will be charged $2.50 for out-of-network ATM withdrawals and $3 for over-the-counter cash withdrawals at banks.

People using the Venmo Purchase Program get extra security for refunds for online purchases. However, there is a 3% fee for sending money to people through the program.

Now, let’s get into PayPal.

With PayPal, things are more complicated. That’s because PayPal has a larger space in other services.

While it’s true that Venmo can be used for some online purchases, PayPal is MUCH more widely accepted in all sorts of stores.

Online, offline, big and small—PayPal is everywhere, even when you don’t think it is.

So the fees for purchasing online or in-store in the U.S.?

There are none.

If you’re transferring money from PayPal to your linked bank account, there’s also no charge. Like Venmo, the basics are free, but there is a 1% charge if you want to make an instant transfer.

Sending money in the U.S. has no charge, if it’s funded by PayPal Cash or a linked bank account.

But here’s where it differs from Venmo:

If your payment is funded by a credit card OR debit card, or PayPal Credit, there’s a 2.9% fee as well as a fixed fee depending on the currency.

When you send to other countries, the rates are even higher:

There are some special cases, but usually anyone sending money to a person in another country will incur a 5% transaction fee.

Yes, that sounds high, especially compared to NOT having a fee at all, but remember that Venmo doesn’t even handle such international transfers.

Here’s another area where things get more complicated:

You can also use PayPal as a payment processor for YOUR store.

If so, here’s what PayPal’s merchant fees look like:

For most merchants, the 2.9% plus $0.30 is the most common fee.

This may not sound great, but it’s pretty competitive compared to what other payment processors would charge.

And if you use software for building an e-commerce site, you can also expect similar rates.

But that’s the gist for PayPal and Venmo’s pricing.

To recap: the basic services are free, though dealing in credit cards (as opposed to debit cards) invoke higher percentages.

Also, PayPal offers more services in other areas, including a greater ability to checkout in stores, but also has other fees accompanying those services.

Let’s transition now to another major factor in the appeal of these platforms:

Ease of Use

One of the reasons PayPal is so successful, is that it’s provided great services for years while keeping things easy for users.

And Venmo, the upstart, has become very successful for similar reasons.

So the question is, which one does it better?

As you’d expect, I’ll start with Venmo.

Venmo’s overall interface is super simple:

On desktop, this is what the homepage more or less looks like.

At the very top, is a notification giving me the option of reminding my roommate about a requested payment.

Then there’s a little field where I can easily request or send a payment to someone.

And then below that is the thing that makes Venmo stand out:

The social feed.

Whether this is good or bad is up to you. Personally, I don’t care for it. But some like the social-media aspect of Venmo, and if you’re one of them, then that’s a bonus.

Luckily, you’re not forced to participate in the public aspect.

Here’s what it looks like when you request/send money:

As you can see, it’s super simple to do this.

There’s a quick privacy option that can always be changed, and an option to share automatically to Facebook.

When you start typing the field for a person to pay/charge, suggestions come up automatically. You’ll have options of previous contacts, and often Facebook friends if you’ve synced with Facebook.

You’ll first be asked to type an amount—and then the term “for” automatically appears, with the option of typing a little note.

That’s it! It’s really as simple as that.

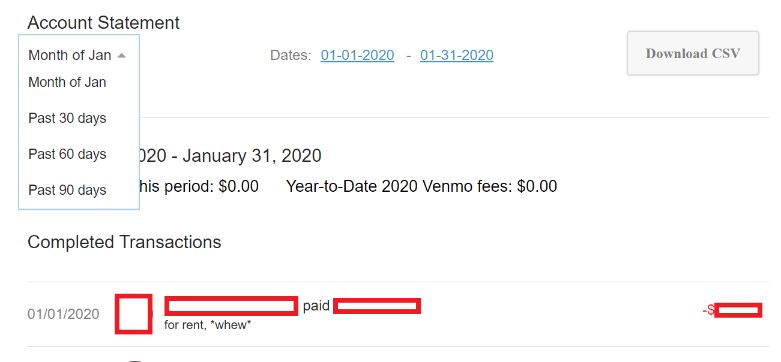

You can also view your previous transactions in an easy “statements” tab:

You can view up to the last 90 days of transactions, and download them if you want to be safe.

Also, usually Venmo transactions will show up in your email inbox unless you opt out, so the record is never completely gone.

Anyway, that’s the gist of Venmo’s ease of use.

Yes, I’m using Venmo via internet browser on desktop, and most people use the app, but it’s pretty much the same (the app is a little better looking).

It’s obviously super simple—you can get to your priority IMMEDIATELY upon accessing the service, without much navigation.

Now let’s take a look at PayPal.

This is what PayPal’s home page looks like:

As you can see, it’s a bit more complicated, though not by too much.

Whereas Venmo puts most of the focus on a combination of the “pay/request” field and the social field, PayPal shows you a few different things:

It shows you your recent activity, quick options for sending and requesting, and seller tools (not in the screenshot).

In general, PayPal offers similar pages and settings to Venmo. However, it’s more advanced.

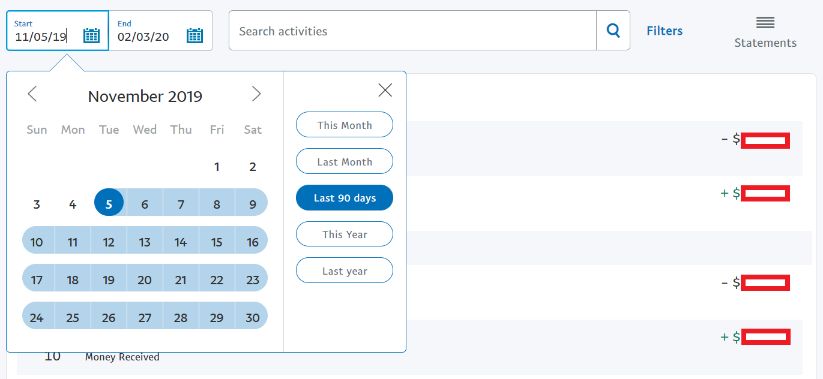

Take this example of activity/transaction history:

You can view activity going back to much longer than the last 90 days—you can view activity going back YEARS.

You can also search for certain transactions or filter them by type.

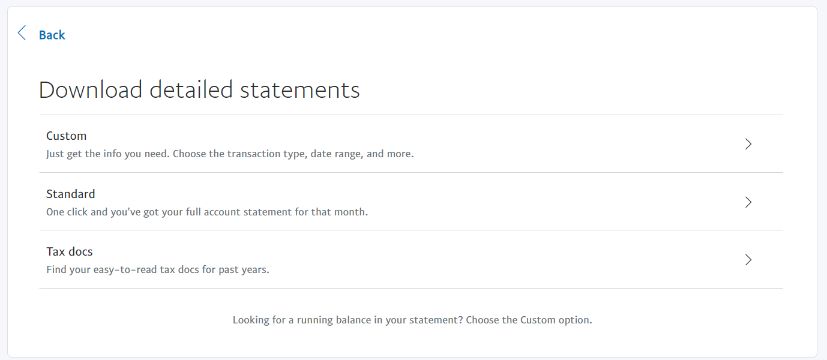

Best yet, instead of a simple option to download a general record for a given time, you can generate and download more detailed types of statements:

This is really cool, and is a case in point of how PayPal provides more advanced features while still keeping things simple.

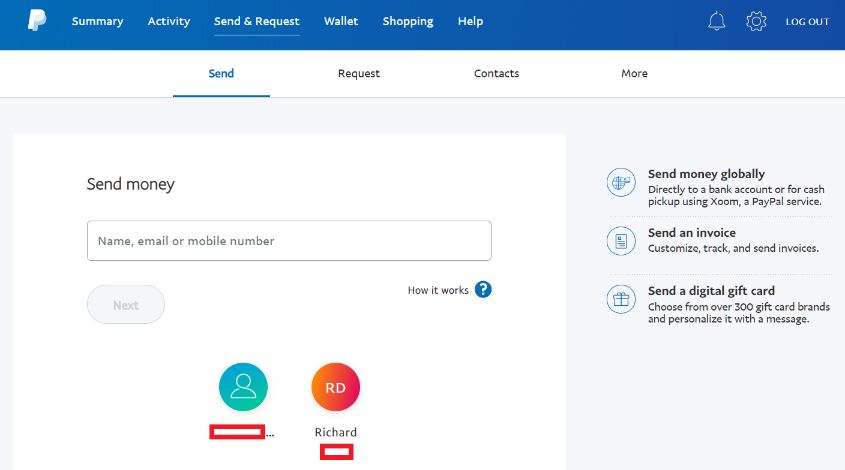

The same thing goes for the basic send/request money feature:

It’s still really simple, but it does involve a couple more steps than Venmo.

Again, this is the desktop/browser version of PayPal, not the mobile one—but the gist is about the same.

My concluding remarks on ease of use probably won’t surprise you:

Venmo is easier in general, because it’s simpler.

PayPal is more complicated if you just want to send and receive money between people you know.

But if you want to take advantage of multiple services, then PayPal does a great job of combining ease of use with features.

Now let’s talk about one last point of comparison:

Security

Security has to be important to you here, even if it’s not the first thing you think of:

After all, you’re trusting these apps with your MONEY! And not just that, but a connection to your bank accounts and card numbers!

So let’s dive in.

Venmo has a page on its site where it just talks about security.

Unfortunately, it doesn’t say much.

For example:

This sounds good, of course—I’d much prefer Venmo use encryption than not.

But this isn’t an exceptional layer of security—it’s good basic security in 2020, but something most major sites and online services do.

Since Venmo is handling money for millions of people, I want to see more.

Now, Venmo does have some security tools that are simple, but useful, like this:

In your account settings, you can edit your remembered devices and sessions (where you’re currently logged into Venmo).

If you lose your phone or it gets stolen, you can remove it so it can’t be accessed.

You can also add in password requirements to use the app on your phone.

So ultimately the basics are there—the servers are secured, the traffic is encrypted, and users can protect their account.

I wish there was more, but it’s not too bad.

But let’s switch gears to PayPal: it’s even more important for PayPal to have great security, since it’s becoming more of a bank/card.

There’s one thing about PayPal and security that’s pretty underrated:

The ability to checkout with PayPal on countless websites online (and even in-person stores).

One might wonder why they’d check out with PayPal when buying something online, when they can just use their card—isn’t it more complicated?

Well, actually, it’s not.

When you check-out on a site through PayPal, you only need your PayPal login info—you don’t need to enter your entire card number and billing information.

But better yet, it’s more secure:

You’re not trusting the store with your card and billing info—you’re just trusting PayPal to do the transaction for you.

And PayPal monitors all transactions in case something goes wrong:

So this is a great point in favor of security.

PayPal also does this for businesses—making it a great payment gateway option if you’re running an online store.

The thing is, this 24/7 fraud detection goes for just about everything you do on PayPal.

This means that even just sending and receiving money falls within this purview—so it’s not like you only get this protection for buying and selling online.

PayPal also offers security settings for users like Venmo (or rather, Venmo has similar settings to its owner, PayPal):

Although I will note here that PayPal’s settings are a little more advanced.

Now, I need to be fair to Venmo:

Venmo DOES allow people to make purchases online through the service.

But a large part of that is through PayPal: when you checkout online, you can pay using the PayPal button…using your Venmo account.

And as this is the case, it’s subject to similar monitoring.

The more practical application is using Venmo for in-app purchases.

But even so, PayPal is simply more widely accepted in stores, and to the extent Venmo is secure for online purchases, it’s mostly attributable to PayPal.

With that plus more advanced user settings and a much more established reputation, I’ve got to say that PayPal has better security.

Let’s recap all these pros and cons before wrapping up:

Venmo Pros and Cons

Venmo Pros:

- Free to install and use

- No fees for basic services, like: sending money from a linked bank account, debit card, or Venmo balance, or for receiving and withdrawing to your account.

- Simple and easy to use.

- Although Venmo is still overall simpler in what it offers than PayPal, the introduction of the Venmo card is a nice step and a good option for people already using Venmo.

- The social nature of Venmo is good for those who like it, but can be easily disabled for those who don’t.

Venmo Cons:

- Only available to those in the United States

- Transfer limits are lower than PayPal’s, though still in the thousands per transaction.

- Not as widely accepted as a checkout option as PayPal.

- Not as robust security/monitoring systems for online purchasing, compared to PayPal.

PayPal Pros and Cons

PayPal Pros:

- Free to install and use.

- No fees for the basic services of sending and receiving (similar to Venmo).

- Can be used worldwide.

- Higher limits on how much can be transferred at a time.

- PayPal has more business-related features (especially as a checkout option/payment gateway).

- Aside from being useful for businesses, consumers can use PayPal as a checkout option as a safe way of paying for things on potentially risky sites, and getting monitoring for refunds.

- Also offers loans.

- Overall, more complex settings and tools.

PayPal Cons:

- Fees for sending/receiving outside of your country (note that Venmo is only for U.S. users, so comparatively it’s not such a drawback).

- For those who just want to send and receive money with their friends and acquaintances, PayPal is likely overbearing.

Venmo vs PayPal: Which is better for small businesses and freelancers?

I just want to focus on this for a bit before wrapping everything up in the conclusion.

Basically, PayPal is better for businesses. It has more tools and features that make it naturally more suited to handle business transactions.

I’ve used both to accept freelance payments, and I think each has a thing they’re better at, though.

Here’s where Venmo is best:

If your freelancing work involves smaller jobs and relatively smaller amounts of cash, including one-off payments, then Venmo’s ease is a pleasure to deal with.

Also, a lot of clients may find Venmo to be easier to deal with.

It’s extra good for jobs you do for friends or people in your circle.

Aside from that, PayPal is overall better, though.

For one thing, transaction records last longer and can be assessed in more detailed ways, including with tax information.

If your small business is an online store, or if you’re thinking of branching into e-commerce, then PayPal is almost certainly the better choice.

This is because it can be used as a payment processor, and many reputable sites/services already use PayPal on their websites as a checkout option.

Okay, ready to wrap up?

Which is better: Venmo vs PayPal?

Which is better, in general?

I’d have to say PayPal is better overall.

At the end of the day, it does more or less the same thing as Venmo…but much more when needed. And the basics cost the same.

And is that extra complication really so bad? Not to me, and not to most of you.

And as I discussed in the last section, PayPal is by far better for business, unless you’re running a small, local freelance operation.

BUT, here’s an important bit of nuance:

I use Venmo much more than I use PayPal.

Why?

Because the vast majority of people in my life use Venmo over PayPal. That alone makes it much more worth using.

So on paper, PayPal may be the much better choice. But in practice, for those in the United States, Venmo is often the more practical one.

Unless, I repeat, you are running a business!